Corporate Transparency Act — Beneficial Ownership Information Reporting Requirement

Starting January 1, 2024, many businesses will be required to comply with the Corporate Transparency Act (CTA). The CTA was enacted into law as part of the National Defense Act for Fiscal Year 2021. The CTA requires disclosing the beneficial ownership information (otherwise known as “BOI”) of certain entities from people who own or control a company.

It is anticipated that 32.6 million businesses will be required to comply with this reporting requirement. The BOI reporting requirement intends to help U.S. law enforcement combat money laundering, the financing of terrorism, and other illicit activity.

The CTA is not a part of the tax code. Instead, it is a part of the Bank Secrecy Act, a set of federal laws that require record-keeping and report filing on certain types of financial transactions. Under the CTA, BOI reports will not be filed with the IRS but with the Financial Crimes Enforcement Network (FinCEN), another agency of the Department of Treasury.

Below is some preliminary information for you to consider as you approach the implementation period for this new reporting requirement. This information is meant to be general-only and should only be applied to your specific facts and circumstances with consultation with competent legal counsel and/or other retained professional adviser.

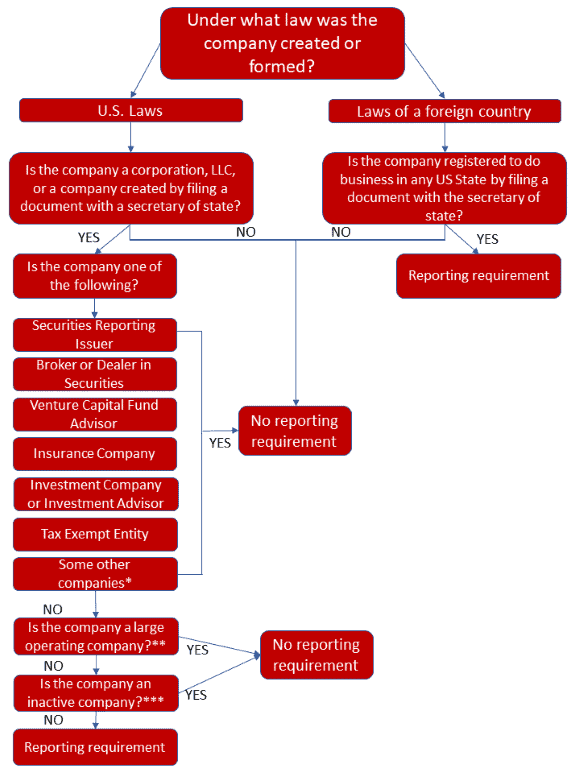

What entities are required to comply with the CTA’s BOI reporting requirement?

Entities organized both in the U.S. and outside the U.S. may be subject to the CTA’s reporting requirements. Domestic companies required to report include corporations, limited liability companies (LLCs), or any similar entity created by filing a document with a secretary of state or any similar office under the law of a state or Indian tribe. The reporting requirements are expected to apply to most small business entities with less than 20 employees or with less than $5M of gross revenues unless they are specifically covered under other specific exemptions.

Domestic entities not created by filing a document with a secretary of state or similar office are not required to report under the CTA.

Foreign companies required to report under the CTA include corporations, LLCs, or any similar entity formed under a foreign country’s law and registered to do business in any state or tribal jurisdiction by filing a document with a secretary of state or any similar office.

Are there any exemptions from the filing requirements?

There are 23 categories of exemptions. The exemptions list includes publicly traded companies, banks and credit unions, securities brokers/dealers, public accounting firms, tax-exempt entities, and certain inactive entities, among others. Please note that these are not blanket exemptions, and many of these entities are already heavily regulated by the government and thus already disclose their BOI to a government authority.

Below is a chart for additional information regarding exemptions.

*Other Exempt Entities Include – Depository institution holding company, Money services business, Securities exchange or clearing agency, Other Exchange Act registered entity, State-licensed insurance provider, Commodity Exchange Act registered entity, Public utility, Financial market utility, Pooled investment vehicle, Entity assisting tax exempt entity, Subsidiary of certain exempt entities, Governmental Authorities, Public Accounting Firm, and Bank or Credit Union.

**A company qualifies as a “Large operating entity” if all of the below conditions are met:

- Employs 20 or more people in the U.S.

- Has reported gross revenue (or sales) of $5million or more on the prior year’s tax return; and

- Has physical presence in the U.S. – owns or leases office space, regularly conducts business in the U.S.

***A company qualifies as an “Inactive entity” if all of the below the conditions are met:

- Must have been in existence on or before January 01, 2020

- Entity is not engaged in active business

- Entity is not owned by a foreign person whether directly or indirectly

- No ownership changes in preceding 12 months

- Not sent or received funds exceeding $1,000 during the preceding 12 months

- Entity does not hold interests in any U.S. or foreign corporation, LLC or similar entity

Who is a beneficial owner?

Any individual who, directly or indirectly, either:

- Exercises “substantial control” over a reporting company or owns or controls at least 25 percent of the ownership interests of a reporting company.

- An individual has substantial control of a reporting company if they direct, determine, or exercise significant influence over important decisions of the reporting company. This includes any senior officers of the reporting company, regardless of formal title or if they have no ownership interest in the reporting company.

The detailed CTA regulations define the terms “substantial control” and “ownership interest” further.

When must companies file?

Different filing timeframes depend on when an entity is registered/formed or if there is a change to the beneficial owner’s information.

- New entities (created/registered after 12/31/23 but before 01/01/2025) must file within 90 days.

- New entities (created/registered on or after 01/01/2025) must file within 30 days.

- Existing entities (created/registered before 01/01/2024) must file by 01/01/2025

- Reporting companies that have changes to previously reported information or discover inaccuracies in previously filed reports must file within 30 days.

What sort of information is required to be reported?

Companies must report the following information: full name of the reporting company, any trade name or doing business as (DBA) name, business address, state or Tribal jurisdiction of formation, and an IRS taxpayer identification number (TIN).

Additionally, information on the entity’s beneficial owners and, for newly created entities, the company applicants of the entity is required. This information includes — name, birthdate, address, unique identifying number, issuing jurisdiction from an acceptable identification document (e.g., a driver’s license or passport), and an image of such document.

Risk of non-compliance

Penalties for willfully not complying with the BOI reporting requirement can result in criminal and civil penalties of $500 per day and up to $10,000 with up to two years of jail time. For more information about the CTA, visit https://www.fincen.gov/boi-faqs.

Please get in touch with your attorney or legal counsel for more information and assistance with filing these reports.